Benchmark sur l'application d'IFRS 9 par les assureurs européens

La nouvelle norme IFRS 9 sur les instruments financiers est entrée en vigueur le 1er janvier 2018 pour la plupart des sociétés, mais les groupes d'assurance ont la possibilité de reporter son application à 2021, année où la nouvelle norme IFRS 17 sur les contrats d'assurance entrera en vigueur. Découvrez notre benchmark européen (étude en anglais).

IFRS 9 introduces numerous changes (Phase 1/ classification, Phase 2/ impairment, Phase 3/ hedge accounting, disclosures) and its implementation is complex.

We chose to study the 2017 year-end financial reports of 16 European insurance and reinsurance Groups with the aim of identifying trends, progress and the impact they expect on their financial statements when first applying IFRS 9, and sources of these impacts.

Our Sample

We also had a look at a sample of European bank insurers to see whether they are planning to defer the application of IFRS 9 for their insurance activities.

Our Findings regarding (re)insurers

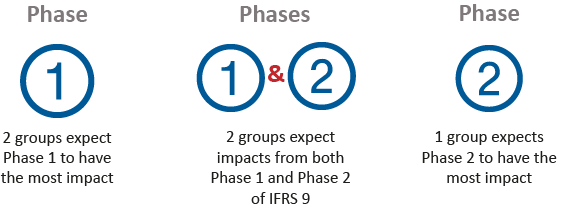

Impact of Different Phases

We have also analysed the expected IFRS 9 impacts by phases that (re)insurers had opted for deferral to 2021. Among the 5 groups distinguishing between the impacts of different phases* of IFRS 9, the main findings are as follows:

*Phase 1 of the standard introduced new requirements for the classification and measurement of financial instruments;

Phase 2 of the standard introduced new impairment principles;

Phase 3 of the standard introduced new rules for hedge accounting.

Interested to find out more about the publication? Download the full study below.

Egle Mockaityte

Denise Wipf Associée - Responsable Assurance Zurich

Related Content

Quantified impacts of IFRS 9: initial findings

At the end of February 2018, all the major European banks published information on the impact of the implementation of the new standard IFRS 9. IFRS 9 introduces numerous changes (classification, impairment, hedging, etc.). Their impacts at the transition date vary widely from one bank to another. They are negative in most cases, but for some banks are virtually nil or even positive. The indicators...

Study on Reinsurers’ Financial Communication 2018

Reinsurance, also known as the “ insurers’ insurance ”, plays a key role in the global market economy today. Several factors, such as the strengthening of capital requirements, the increasing level of significant NAT CAT events or the need for optimal coverage is increasing the need for reinsurance.